Many personal finance headaches stem from a simple budgeting issue (or the lack of a budget entirely)! If you keep finding yourself running short of money to last until payday, you may even question whether budgets work at all.

Managing your own money can sometimes feel like a juggling act 🤹♀️ And it gets even trickier if you’re taking care of household finances too!

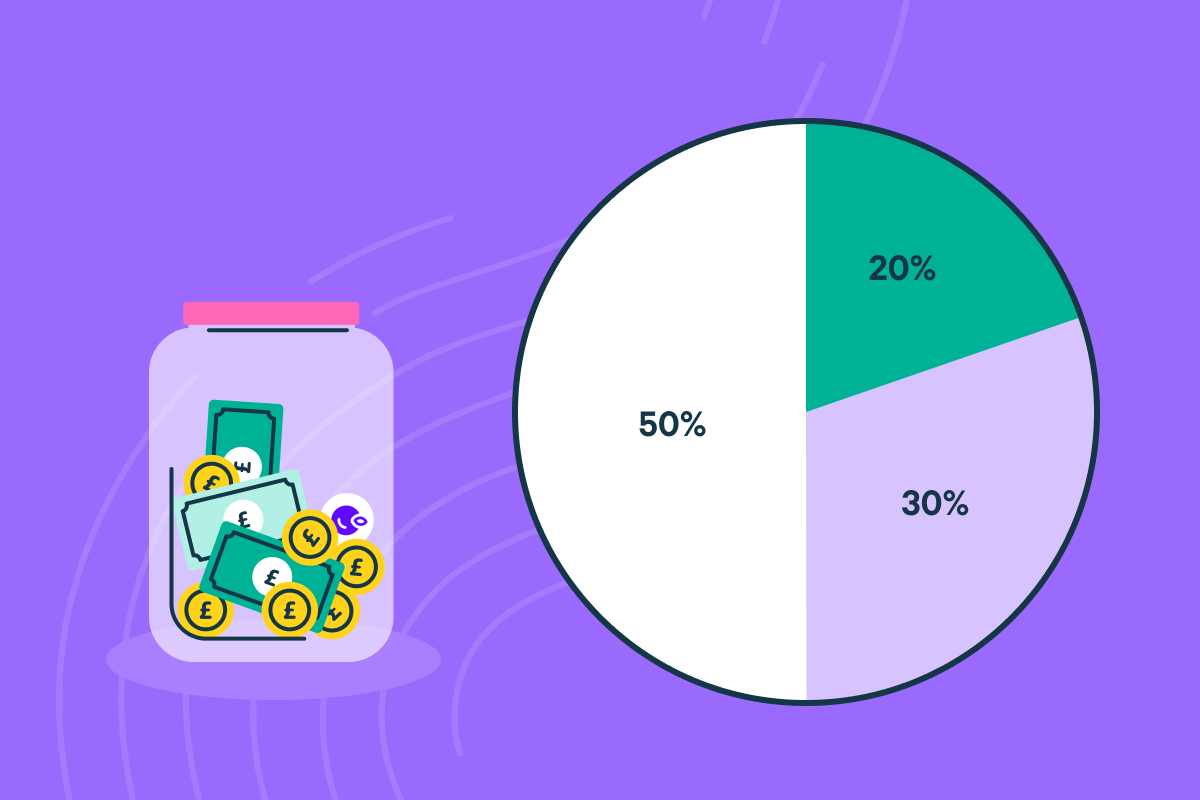

We could all use a little guidance sometimes, and that’s where tried-n-tested budgeting rules can provide a useful starting point. There are lots out there, but the 50/30/20 Rule is versatile because it adapts to your income.

What is the 50/30/20 Rule?

The 50/30/20 Rule suggests you allocate 50% of your take-home salary to your needs, 30% to your wants, and the remaining 20% for your future.

Sounds great in theory. But is it manageable in practice?

We’re here to help you decide if this is the budgeting rule for you!

Essential Needs: 50%

50% of your after-tax monthly income should be allocated for your needs.

This category sounds as though it should be clear-cut. However, as you build your budget you may find you need to make some tough judgement calls 🧑⚖️

Housing (rent or mortgage payments) and utilities are easy to identify. As are the minimum payments on any outstanding debt that you might be carrying. But there are some other ‘essentials’ that could become more of a grey area.

You probably rely on some form of transport to commute to work, and that should be included as essential. Your budget shouldn’t be so strict that you can’t afford to catch the bus, but a reliance on Ubers is harder to justify 🚕

Although food shopping should also be considered a ‘need’, you may need to cut down on the gourmet treats if you’re going to make your budget work

Your Wants: 30%

30% of your post-tax salary should be reserved for lifestyle choices 🛍

You’re free to splurge on holidays, eating out, entertainment or hobbies. Whatever you like… so long as you stay within your 30% budget.

As you calculate the monthly budget for your ‘wants’, you might find more choices and potential overlaps with what can be considered an ‘essential’.

In the modern world, it’s probably fair to consider your mobile phone a necessity 📲 After all, how else are you going to use your Plum app?! And if you feel that having the latest, state-of-the-art phone is important… well that’s a perfectly legitimate decision too (it’s your budget, remember!).

In this situation you can consider assigning the price of a basic mobile phone to your allocated essentials, and any additional expense incurred for a more prestigious model counting towards your wants or lifestyle choices 💁♀️

You could apply this same principle as far as the difference in price between buying supermarket own-brand baked beans and a better known variety.

Finally, when budgeting for your weekends, remember this calculation:

52 Weeks / 12 Months = 4.33 Average number of weekends in a month

So, to avoid being left short the next time a month containing five weekends rolls around… make sure your budget accounts for this 📆 You'll also need a way to stash any money you didn’t spend when you have a little extra to spare.

Your Future: 20%

20% of your take-home pay should be reserved for your long-term future.

Before setting money aside, you first need to tackle any debt (aside from your student loan), but once you’ve cleared the credit card balance or overdraft, the aim is to create a store of money and to protect it from the effects of inflation.

If you’re not sure where to begin, then our earlier article on the basics of personal finance could be a useful source of inspiration.

For example, you could begin by building up an emergency fund to help protect you from financial instability, or investing in the stock market.

Is the 50/30/20 Rule realistic?

Taken out of context, these percentages can feel like abstract concepts.

The rule sounds sensible, on paper. But what about applying it for real? Is it truly possible to cover all your essentials with just half your wages, limit the fun stuff to less than a third… and still have a fifth left over for your future 🤔

Of course it is possible, but whether it’s feasible will come down to your own personal situation, and also how badly you want it!

Even if you can’t make the suggested ratios work straight away, you’ll still be learning an invaluable lesson in money management.

Is the 50/30/20 Rule any good?

Like many things related to personal finance… the answer to this question is ultimately subjective. There is no, one-size-fits-all approach. Whether the rule is ‘good’ will depend on your own circumstances, and that’s not for us to say.

However, although the actual results may vary, the 50/30/30 Rule is so widely applied because it’s a relatively universal rule-of-thumb 👍

You may need to tweak the ratios a little to fit with your life… and that’s ok!

The most important thing is that you’re engaged with the budgeting process. If the rule helps you achieve this, then in our book you’re already winning 🎉

If you'd like to learn more about Plum can help you achieve your goals then you can check out our website.

Download PlumFor all the latest Plum news and discussion, keep an eye on our Facebook group, Plum Squad, or follow us on Instagram and Twitter.